Hello to all my readers. I hope you all are having a gala time out there in the markets, as these roller coaster rides presents us with great opportunities to buy some good company at a bargain price.

Let me share with you one such company who’s making a focused roadmap for its future growth and wanting to make it big in Indian Consumer Durables Market.

Hitachi Home & Life Solutions (India) Ltd

About the company

Hitachi Home & Life Solutions (India) Ltd is a subsidiary of Hitachi Appliances Inc, Japan. Hitachi manufactures various kinds of products including Room Air-conditioners and Commercial Air-conditioners, and is into trading of VRF Systems, Rooftops, Chillers, and Refrigerators.

Headquartered in Ahmadabad, Gujarat, the company's manufacturing facility at Kadi, Gujarat, is among the ten Hitachi air-conditioner facilities worldwide. With a total installed capacity of 400,000 units in a year, Hitachi is amongst the top air-conditioning companies in India.

It has a strong nationwide distribution with presence in 236 town (plans to increase this to 300 cities) consisting of 18 Branches, 159 Exclusive Sales and Service dealers; more than 1800 Showroom dealers (plans to increase it to 3000 by end of 2011), 350 Service Points along with 32 company owned and operated service centers-manned by 1200 technicians.

Product portfolio

The company has a presence in Air Conditioners and Refrigerator markets.

AC Category | Products |

Room Air Conditioners | Window AC, Split AC, Tower |

Packaged Air Conditioners | Concealed Splits, Ductable, Ceiling, Cassette |

Spacemaker | Specific Telecom Cooling Solution |

Setfree | Variable Refrigerant Volume System |

Chillers | Large Air-Conditioning Application |

Refrigerator Category | Products |

Refrigerators | 3 Door Refrigerators |

2 Door Refrigerators | |

Big French |

For further specification of each product you can click here. As per the company its products are technological advance and superior in the market compared to other products. For details you can click here

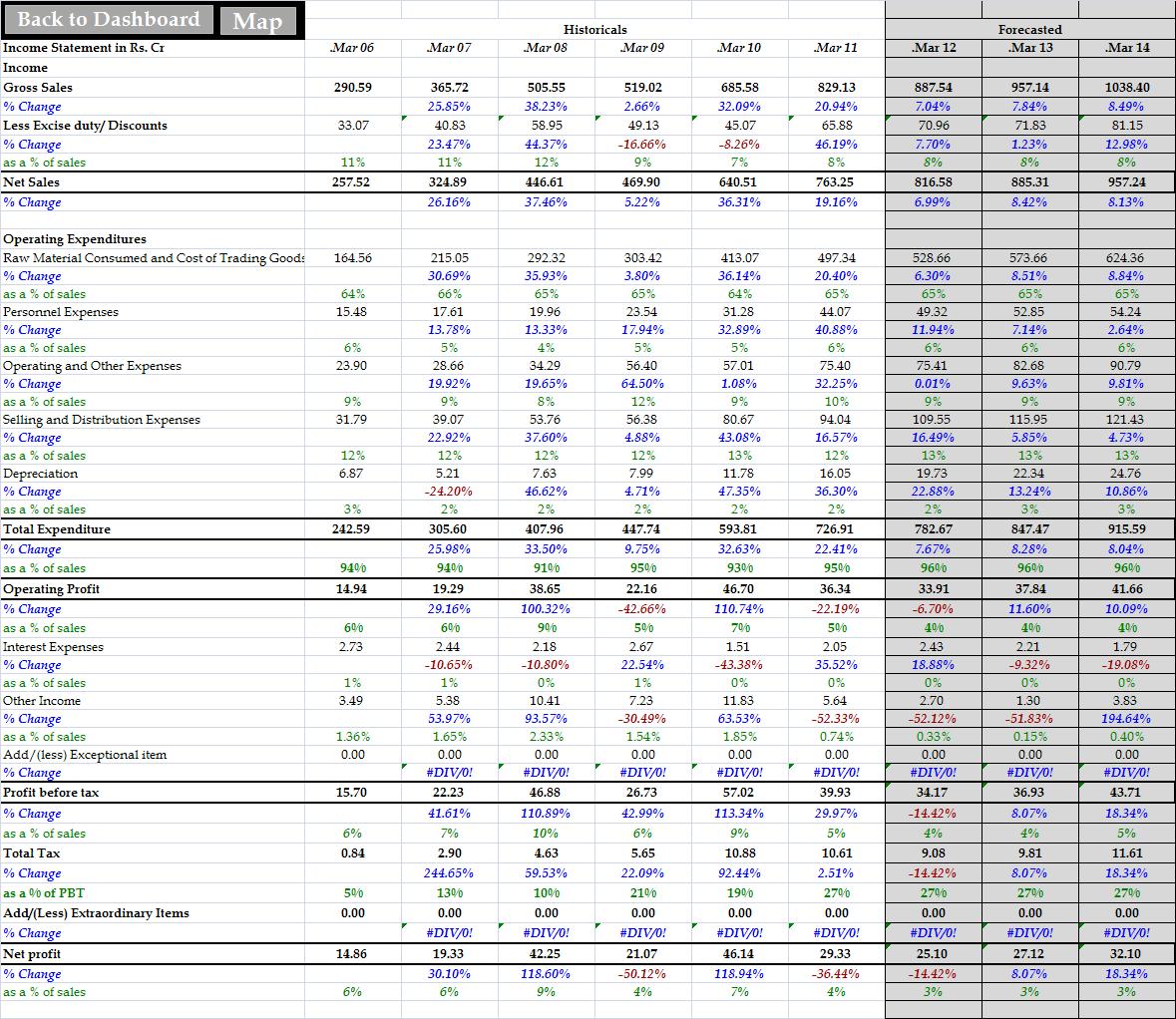

Historic Analysis

Segment and Revenue analysis

- Hitachi is majorly into selling various types of Air-conditioners. It has an installed capacity of 150000 units which was increased to 230000 units in FY10 (single shift basis). It has increased its production from 86874 units in FY06 to 268699 units in FY11 at a CAGR of 25%.

- Total units of Air-conditioners sold have shown an increasing trend every year from 101348 units in FY06 to 243365 units FY11 showing a CAGR of 19%. Selling price per unit has shown an increasing trend from Rs. 26600 FY06 to Rs. 33700 in FY09 and than started showing a decreasing trend to Rs. 29000. Total sales from Air-conditioners segment have grown from Rs. 269.91 cr in FY06 to Rs. 707.20 cr in FY11 growing at a CAGR of 21%.

- Hitachi is also into trading of Refrigerators which is mainly targeted for premium segment in the market. Total units sold have grown at an impressive CAGR of 76% from 843 units in FY06 to 14432 units in FY11. Selling price per unit has increased from Rs. 27900 to Rs. 35400 in the last 6 years which translated into sales of Rs. 2.35 cr to Rs. 51.08 cr growing at a CAGR of 85%.

- Hitachi also generates revenues from providing after sales services. With growth in the products the service revenues has also grown over the years and contributes around 6% of the total sales.

- On a consolidated basis in the last 6 years Hitachi has increased its top-line by 24% CAGR with Air-conditioners and Refrigerators being the major revenue contributor to the company.

Income statement analysis

- Raw material and traded goods cost is the major expenditure for the company. Over the last 6 years this cost has been around 65% of sales. The growth in this cost has been in line with the growth in sales.

- Selling and distributions cost has been around 12% to 13% of sales followed by operating and other expenses with 9% to 10% of sales.

- Over the last 6 years company has constantly upgraded its product portfolio and increased its reach in the market, due to which the cost has been on the higher side for the company. Total expenditure has been around 94% to 95% of sales.

- This has translated into the operating profit margin of around 5% followed by net profit margin of 4% on an average for the company.

- Over all the company with introduction of new product and technology and with changing demand scenario has managed to grow its top-line impressively in the last 6 years but due to increasing cost structure and setting up its base for future growth the bottom line has failed to show an impressive performance for the company.

- Hitachi has financed its growth from internal accruals as well as from outside debt. In the last 3 years it has invested around Rs. 132 cr in its fixed assets and generated an average return on fixed asset of 32%. Additional plant was built adjacent to its old plant in FY10 for manufacturing of Air-conditioners and also opened several services centers in the country.

- Inventory as a % of sales has been on a higher side at 28% to 30% on an average due to seasonality of the business as the company needs to keep the stock of finished goods in summers. In FY11 the inventories has increased by a whooping 82% due to extended winters and early rains which hampered the sales of goods. This impacted the cash flow from operations and resulted in reduced cash balance for the year. Receivables have been managed reasonably in line with sales.

- Creditors have also shown an increasing trend, financing the major part of current assets of the company. Thus current ratio has been well maintained at an average of 1.3 times historically.

- Its current Debt/Equity ratio stands at 0.52 which is at a comfortable level. Increase in debt from Rs. 60 cr to Rs. 90 cr was mainly to finance its working capital requirement. Hence the Debt/Net profit ratio stands at 3.07 which is not a big cause of concern.

- It has increased the shareholders fund from Rs. 61.8 cr to Rs. 172 cr in the last 6 years with CAGR of 23%. It has paid a dividend of Rs. 1.5 for FY11.

- Hitachi has constantly improved the product offering in terms of latest technology and introducing new product in the market which has helped them achieve an ROCE and ROE of 21% and 30% on an average respectively in the last 6 years.

- On a consolidated view the balance sheet does not pose much problem for the company has it has managed well to finance its fixed assets and increase the shareholders fund at a decent rate. Except for growing inventories (due to seasonality reason) the overall picture looks decent.

Improving demand scenario:

- The Indian retail market, which is the fifth largest retail destination globally, has been ranked as the most attractive emerging market for investment in the retail sector. The organized retail sector is all set to witness maximum number of large format malls and branded retail stores in the next two years. Organized retail would not only streamline the supply chain, but also facilitate increased demand, especially for high-end and branded products.

- Indian Air conditioning industry is experiencing a radical change since last few years. There are several factors favoring the Indian Air-conditioner market growth. Changing lifestyles, rise in disposable incomes and the ease of availability will increase the Air-conditioners penetration in future. Room Air conditioner penetration in India is at approx 3% which is very low compared to other countries like China, Malaysia, Korea, Taiwan etc. It is expected to grow up to 5% by 2015.

- Hitachi has healthy brand equity in the Air-conditioners market wherein it is positioned as a high‐end and premium brand. Hitachi has always pioneered in technology and innovation and has been ahead of the competition in introducing newer concepts and features in air-conditioning due to its high spending on R&D. This has enabled them to achieve higher growth in all the areas it operates.

- In Room Air-conditioner segment it has been able to grow at 46% over the last year with 2.3 lacs unit against 1.58 lacs unit. In the Commercial Air-conditioners market it has shown a positive trend by growing at 11% in Ductable air-conditioner segment. In Chiller and VRF segments it has managed to grow above industry growth rate. In Telecom Air-conditioner segment it has maintained its leadership position with the market share of 42%.

- From next year onwards BEE is making the star rating system more stringent, which means the EER of all star ratings will go up. Therefore to qualify to be a 5 star Air conditioner the minimum EER will be 3.3, which is 3.1 at present. Hitachi currently offers higher EERs in all the models therefore it will easily adapt to the new system with ease.

- The company is improving its services by opening up of various service centers across the country with employing trained workforce thus improving the after sales services resulting in better customer satisfaction.

- Thus brand Hitachi appears to be better placed among white-goods makers as it has shown a strong and committed focus to grow and create value for the company in the coming future.

- Hitachi, which has been only in the premium air-conditioner market, is now making inroads into the mass-premium category. In FY10 it entered into mass premium range of Split and Window Air-conditioner with launch of Kaze series targeting the fast growing niche segments of the Tier-II and Tier-III cities, where buying power is on the rise.

- Following the success of ‘Kaze’ series last year it launched a new variant ‘i-clean' series of Split Air-conditioners and India’s first ever 5 star rated Window Air-conditioner ‘Summer’. It also launched new models of its popular Split Air -conditioner models ‘ACE Followme’, ‘ACE Cutout’ and ‘i-Tec’, with new looks and advanced features. Now Hitachi’s Split Air-conditioners range comprises of 25 models, with capacities ranging from 0.9 Tr. to 3.5 Tr. Class. The Window Air-conditioner range includes 10 models within 1 tonnes to 2 tonnes class capacities.

- Hitachi has also introduced various new series of Refrigerators. It has 16 models in 3 variants i.e. Big French (4-Door), three door and two door refrigerators. Company operates in 300 Liters and above frost free segment only which is only 15% of total refrigerator industry. It focuses only in premium category therefore the huge sales volume is not expected. However it has shown very encouraging growth historically and is expected to do well as market conditions improve.

- It is planning to re-enter the Indian market for washing machines with a range of top-and front-loading washing machines in the coming months which will further increase the top line of the company.

- Hitachi enjoys a share of 7.5% in the room air-conditioner market in India and plans to increase this to 10% by FY12 and 15% by FY15. It has build a strong nationwide distribution with presence in 236 town (plans to increase this to 300 cities) consisting of 18 Branches, 159 Exclusive Sales and Service dealers; more than 1800 Showroom dealers (plans to increase it to 3000 by end of 2011), 350 Service Points along with 32 company owned and operated service centers-manned by 1200 technicians. With these stations fully operational now, it will boost the sales in a big way in the coming future.

- Increase in commodity prices like steel, copper, aluminum is forcing all the manufacturers to increase the price. Freight cost and increasing operating costs will increase the over all cost. Because of BEE standards of Energy efficiency the specifications of all Air-conditioners are going up which results in the cost increase.

- The cost of finance is going up and Banks/NBFCs are tightening their norms to take exposure on consumer finances, consequently the funding options have minimized. Inventory funding is also very tight, which is not a good situation for intermediaries to run their operations.

- High electricity cost & consistency in power supply remain a hindrance in the growth of business. Long power cuts and voltage fluctuations may affect the pace of industry growth.

- The import of low cost products from neighboring countries continues to be a threat to the consumer durable industry.

- Growth in Real estate has been subdued which is a negative sign for consumer durables sector.

- Increased competition from other organized players Voltas, Onida, LG, Samsung, Whirlpool and others will result in stiff competition and also face pricing pressure.

What If Scenario?

Now this is a very interesting section of my analysis. Here I try to find out the worth of the company if things don’t turn out to be very hunky-dory and company has to face tough times in the foreseeable future. Through this approach one can get a fair idea of the entry point in the stock and reduce ones risk from buying at higher price. So lets look at what would Hitachi value be in such scenario.

Major Assumptions

Income statement

- Sales: In the last 6 years Hitachi has grown at an average rate of 26% and at 24% CAGR. I assume that the sales will grow at 7% to 8% in the next three years.

- Raw materials and traded goods cost: Historically it has grown in line with growth of sales. I assume the same trend to continue and be at 65% of sales.

- Operating profit margin: Historically margins have been in the rage of 5% to 7%. Going forward I assume the operating margin to decrease and be at 4% as cost will increase more than the sales.

- Net profit margin: Subdued sales and increase in cost will result in lower net profit margin. Historically it is in the range of 4% to 6% on an average. I assume the net profit in the coming future to be at 3%.

- Inventories: Inventories in the major portion of current assets. Any changes in this will affect the cash flow from operations. Historically inventories as a % of sales have been in the range of 28% to 30%. It showed a massive increase due to weaker sales in FY11. Going forward I expect the inventories level to be maintain at a decreasing range of 40% to 34% (still higher than the historic range) of sales as market condition start improving.

- Debtors: I assume it to grow in line with sales.

- Creditors: I assume the creditors to remain flat for the forecasted period.

- Fixed Assets: In last 3 years Hitachi as invested around Rs. 132 cr in its fixed assets for increasing the capacity and opening up of services centers. Going forward I assume it will continue to invest in its fixed assets at an average rate of 4% of sales. This is an important assumption as this directly affects the FCF, thus affecting the valuations.

- Total Debt: I assume the company to raise more debt in the current year to finance its working capital and expect to show slight decrease in the coming years.

- I have assumed a 2 stage growth model as I believe the investment made in the last 3 historic periods and in the forecasted period will start giving fruitful result. I assume in the 1st stage of 3 year the FCF to grow by 8% and in the stable period to grow by mere 4% perpetually.

On a consolidated view I have assumed the current year not to be very good for Hitachi and expect the momentum to start picking up slowly in FY12 onwards.

With all the above assumptions we arrive at a DCF price of Rs. 157 against the CMP Rs. 180 as on 8/9/2011 which is based on a very conservative approach.

Considering all the above factors I believe Hitachi has very well positioned itself in the White goods market by building a strong portfolio of products and services with advanced technology and is ready to grab the huge opportunity which India is presenting by expanding its reach across the country. We should see a strong growth in net sales and profit in the coming future.

Fingers Crossed on Hitachi!!!!

How about you?

4 comments:

Sir,

Any view on the September 2011 results?

Neeraj

Hi Sir,

Sept result were very dissappointing and i think dec quarter will be not good as well due to seasonality factor.

But given the expansion plans of the company i think FY12-13 will be good.

So keeping Fingerscrossed :-)

Thanks & Regards

Yogesh

Hi yogesh,

Could you tell me something about BATA INDIA Ltd.

Let me know what to do with this company as i am holding a lot of share of BATA INDIA Ltd.

Thanks & Regards

HARSH

Hello Harsh,

I havent looked at BATA INDIA LTD so will not be able to comment on it.

Thanks for droping by :-)

Regards

Yogesh

Post a Comment