Hello once again to all my readers. As I promised to come up with companies with sound business models and investing opportunities, here I am presenting to you one such company who has been doing a great job in managing its business and increasing the shareholders value year over year. The company which I am talking about is Tata Sponge Iron Ltd. Let us now learn more about this company.

Company Profile:

Tata Sponge Iron Ltd (TSIL) is an associate company of Tata Steel. It is into manufacturing of Sponge Iron. It has manufacturing facility at Bilaipada (in Joda Block of Keonjhar District in Orissa) with total production capacity of 390,000 TPA from 3 kilns. It has 2 captive power plants using waste heat recovery producing 26MV of power and exports its surplus power to the State Electricity Corporation. For this purpose, the company has installed a private 220 KV power transmission line from its plant to the nearest grid station at Joda (7 kms) to facilitate uninterrupted power transmission to and from the Grid (in case of emergency in the plant).

The company's primary product, sponge iron, is a high quality pre-reduced ferrous material and, therefore, is preferred to most other materials in place of steel scrap by secondary steel producers operating induction and electric arc furnaces for producing long products for meeting the demand of the construction and infrastructure sectors. More about sponge iron you can check this link here. For process of making sponge iron you can check this linkhere:

· TSIL has installed capacity of 390000 TPA from 3 kilns and has shown an improvement in performance every year by increasing the capacity utilization from 72% in FY07 to 98% in FY11.

· Total quantity sold has also grown at a healthy rate Y-o-Y as demand from secondary steel makers kept on increasing. The total quantity sold increased from 206665 TPA in FY06 to 380273 TPA in FY11 with a CAGR of 13%.

· The selling price per tonne has increased from Rs 10697 in FY05 to Rs 18388 in FY11 with CAGR of 10%. The price decreased in FY10 due to recessionary factors which were also seen in the prices of raw materials.

· The total raw material cost per unit has shown a consistent increase from FY05 to FY11 except for FY10 ranging from Rs 3842 tonne to Rs 9905 tonne at a CAGR of 17%. Coal accounts for approx 55% of cost with iron ore around 40% to 43% and remaining portion from Dolomite. The total raw material cost per tonne as a % of realization per tonne has shown an increasing trend from 47% in FY06 to 54% in FY11 implying that the increase in cost is more than the increase in realizations.

· In power segment it has an installed capacity of units 227.76 millions KWH. Total units produced as a % of installed capacity has shown an increasing trend from 73% in FY08 to 84% in FY11. On an average the company has sold around 70% of units produced to the state grid and used the rest 30% for captive use. Power segment contributes around 5% to 7% of the total sales.

· With the above developments the total sales of the company had an impressive growth from last 7 years showing a CAGR of 20%. The raw material cost as a percent of sales is around 65% in FY11 which is the major cost for the company.

· Operating profit margins was lowest in FY07 at 7% as net realizations grew marginally compared to huge spike in raw materials cost. Margins were back to normal rate from FY08 at 27% but started showing a decreasing trend from there on to 20% in FY11. This was due to increase in the raw material prices which effected the net profit margins as well, which is been decreasing from last 20% in FY08 to 15% in FY11.

· The contribution from other income and earnings from carbon credit off set the increase in raw material prices to some extent and it was able to maintain the bottom line at a reasonable level.

· TSIL has financed its investments through debt and internal accruals. It has made major investment in fixed assets in FY06 to increase the installed capacity and in FY10 in Radhikapur for development of coal blocks.

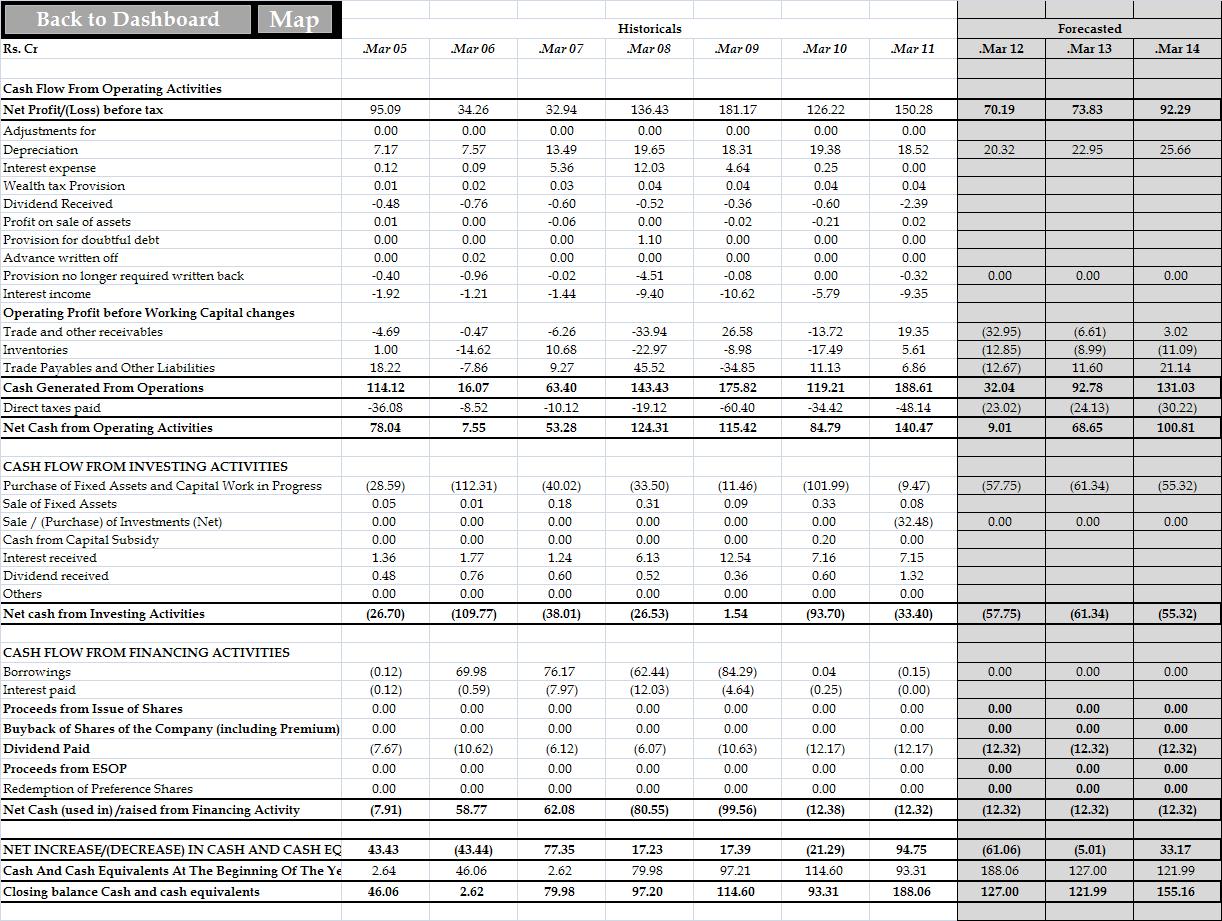

· The company has managed their working capital very optimally which led to increase in cash flow from operations. With this it has paid down all its debt and become a debt free entity from FY09 onwards and currently the cash position stands at a healthy amount of Rs 188 Cr and investment of Rs 34 Cr in liquid funds.

· The way it has managed its operations over the past has reflected in increase in the shareholders fund from Rs. 132 Cr to Rs 508 Cr at a CAGR of 25% from FY05 to FY11. It has also paid consistent dividend to shareholders.

· Over the last 7 years TSIL has paid out 14% of its net earnings as dividend to the shareholders. The rest 86% it has invested back in its business on which it has earned an average return on equity of 27% every year.

Growth Drivers:

Future of sponge iron is linked to the growth of steel demand in country and its fulfillment through secondary steel sector. Growth in the steel demand has strong correlation with growth in GDP of nation. As Indian economy is slated to exhibit robust growth in GDP, steel demand is also expected to grow in tandem. Although there is slowing down of growth in steel industry in the medium term, integrated steel plants still fall short in capacity to meet full demand of steel in India. Secondary Steel sector will continue to play significant role in steel supply in the country. The thrust by the government on infrastructure development gives hope for expansion of integrated steel plants in India.

· In FY05 company had laid down its long term plan of installing 6 kilns along with generating green energy. TSIL has installed capacity of 390000 TPA from 3 kilns and has shown an improvement in performance every year by increasing the capacity utilization from 72% in FY07 to 98% in FY11. Increase in capacity is the only option for the company at this point in time so as to increase their top line. The company is also planning to venture into steel production but given the potential for sponge iron in the coming future I believe the company will focus majorly into making sponge iron.

· The cost of iron ore and coal constitute major cost of production. Therefore the profitability of the company depends on market price of these raw materials vis-à-vis price of sponge iron. The only way to substantially reduce the cost of iron ore and coal is to have captive mines for these raw materials.

· TSIL sources entire requirement from Tata Steel, where it offers some discount to the market prices. Tata Steel supplies iron ore from its Khondbond mines in Orissa, which is 25km distance from TSIL plant thus reducing the transportation cost. A secured source of iron ore is an asset for the company, as quality and quantity is maintained. It also helps to reduce the effect of raw material price volatility and improve margins. It sources Coal from domestic sources through e-auction and imports. The Coal block at Radhikapur is expected to become operational from FY12-13. This will decrease the raw material cost substantially and an assurance of continues supply will help company improve its margins in the coming future.

· Utilization of waste resulting from production of sponge iron to generate power has made a great impact as uninterrupted supply of power is assured and also on financials of the company resulting in additional revenues and better operational efficiencies. The company now plans to recycle waste char (from kilns) to generate power through the AFBC boiler based power plant. However, according to management of TSIL, this is at nascent stage and expected to be operational after FY12-FY13. This will further result in improvement in the sales and margins.

· Improved performance over the years has resulted in strong balance sheet of the company. It has Rs 220 Cr in form of cash and cash equivalents with no debt and addition to this it has around Rs 129 Cr as capital work in progress backed by optimal working capital management has put the company in an advantageous position. Thus it can easily survive in bad conditions and can easily finance its future investment with internal accruals of the company.

Concerns:

· As a pure sponge iron player (95% of revenue) earning is volatile due to inherent volatility in raw material prices. TSIL is procuring all its Iron ore from Tata Steel Ltd, which is the only supplier to the company. Any disruptions in the supply of Iron ore will have a major impact on company operations. Any delays in development of coal field will mean that the company will have to continue to procure the raw materials through imports and from indigenous sources.

· Poor quality of indigenous coal, dumping of scrap by overseas players, recessionary conditions, liquidity crunch in financial markets etc are some of the significant threats being presently faced by the company.

· The infrastructural constraints at ports and rail-rake availability are posing problems in getting imported coal from ports and by rails. The transportation cost is high due to existence of transport union in state of Orissa. All this factors will increase the cost and will decrease the profit margins.

Well the above points does make one believe the way it has performed historically is awesome and various developments expected to take place will certainly improve the company’s performance.

But hey wait a sec… what if history doesn’t repeat itself. With the global crisis going around it does seems things will be very difficult for a year or may be more or may be with such sound management the company will be able to overcome all the hurdles and show a strong performance Will it??

It’s a difficult question to answer.

To make things a bit clear and to reduce our risk and be on a safer side let us assume that things will be very difficult for next two years and work out a scenario where we try to analyze the not so good performance by the company and see where does the company stand if things fall out this way.

Assumptions:

Sales:

· I have assumed that there will be no expansion in the installed capacity for the coming future.

· Production as a % of installed capacity will decrease because of weak market conditions and rise slowly as things get better.

· Total quantity sold will decrease and as a result the inventory will show an increasing trend in the coming future.

· Historically in the past 4 years the selling price per tonne as been in the range of Rs. 14000 to Rs. 18000 on an average. I have assumed that the selling price per tonne will decrease and be around Rs 16500.

· In power segment since it is linked with the production of sponge iron, I have assumed that there will be flat growth in terms of revenues.

· With all the above assumption we arrive at the gross revenue which shows negative growth in FY12 and than slowly picking up with single digit growth.

Raw Materials

Raw materials (Iron ore and Coal) are the major cost for the company and any changes in this will impact the profitability of the company.

· Here I have assumed that the raw material cost will not decrease and will be on a higher side in the future hampering the margins of the company.

Margins:

· Historically the operating profit margin has been in a decreasing trend from 27% in FY08 to 19% in FY11 due to increase in raw material costs. Since we have assumed that the selling price will decrease because of the competition and the raw material cost to keep increasing, the operating profit margins will take a hit and remain in the range from 8% to 13% in the forecasted period as company is unable to pass on this increase to the end customer.

· This will also decrease the net profit margins and assume it to be in the range of 8% to 10%.

Working capital:

I have assumed Debtors and inventories as a % of sales to increase in the forecasted period because of weak market conditions and expect the creditors to be flat putting pressure on company balance sheet which will result in decrease in cash flow from operations for the company.

Fixed Assets

· Here I have assumed the company to keep on investing in its fixed assets for the development of coal block and also the capacity but with execution delays. This is a very critical assumption to make as it directly affects the Free cash flow of the company.

DCF Assumption

· Here I assume a single stage growth model and expect that the company after the forecasted period will grow by mere 2% perpetually.

Alright than now that we have made a roadmap for the coming periods with the above assumptions and being as conservative as possible we get the DCF price of Rs 295. This is the fair value of the company if the above scenario falls in place.

At CMP of 300 as on 30th Aug 2011 we are very close to the fair value of the worst performance of the company. Any revival in the demand scenario and economy should have a positive impact on the company financials and I believe with such great management the company should do well even in the bad times.

I have kept my Fingers Crossed on this idea!!!!

How about you????

7 comments:

Excellent and very very detailed first post Yogesh. Do keep up the great work.

Thank you so much for your kind words..it really boosts my confidence :-)

Awesome Yogesh.. Keep it up..

Hey Yogesh, followed your link from your comment addressed to me on Rohit's blog. You too, have an interesting blog. Your analysis of Tata Sponge is excellent. Hope to become a regular visitor to this one, too besides Rohit's blog.

Thanks a lot for dropping by Sachin :-)

Interesting quarterly results there from TSIL. Splendid operating profits on the back of a decline in sales! Did some interesting management at the raw materials level.

Hi Sachin,

I totally agree with you :-)

Regards

Post a Comment